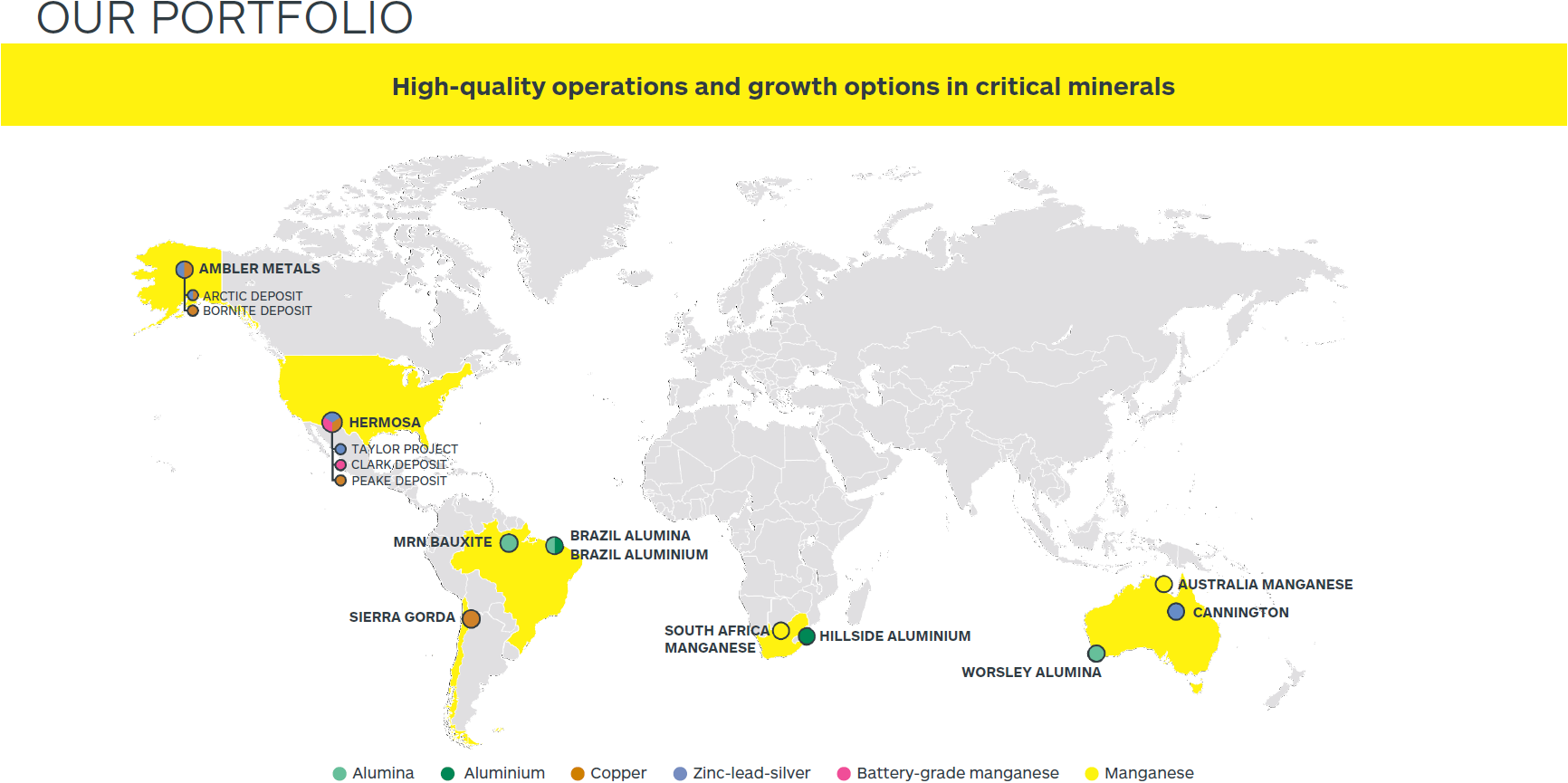

A Portfolio Built for the Energy Transition

South32 (ASX: S32) is increasingly positioning itself around copper, zinc and silver, metals closely tied to electric vehicles, renewable energy and data centre construction. The flagship development project in Arizona, which contains large zinc and silver deposits, has seen costs rise more than 50% to US$3.3 billion, with first production now delayed to late 2028 and full output pushed to 2031. On the other hand, the broader resource has grown by 52%, extending the project’s life to 33 years. Existing operations across Australia, South Africa and South America continue to generate reliable cash flow.

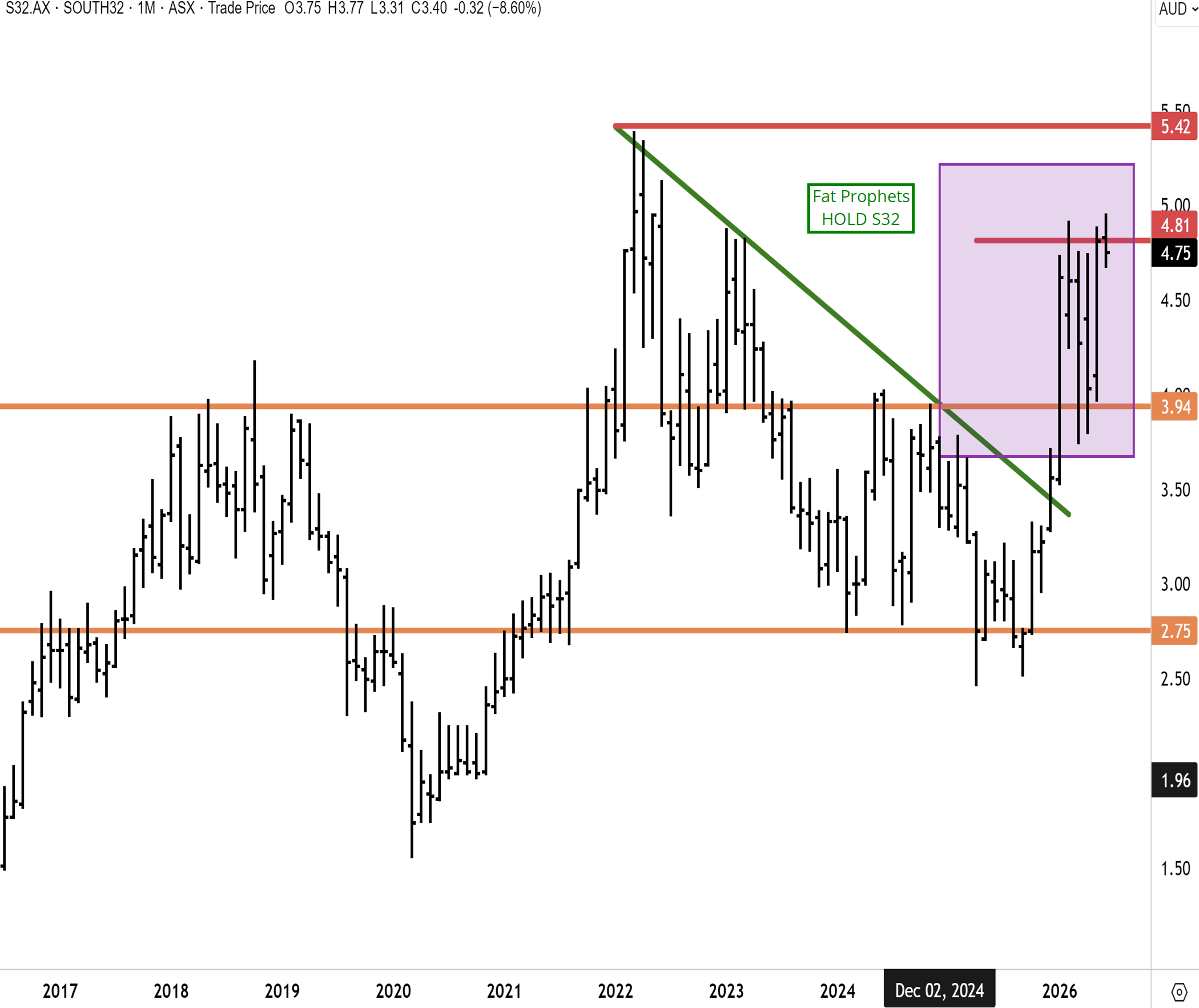

In our last tech update on the 27th of April, we noted that “South 32 continues to consolidate after surging to four-year highs above $4.90 back in February. While S32 corrected lower in March, it was a ‘risk off’ environment for global stock markets, and upward momentum has since resumed. We believe the correction that unfolded last month is close to ending. Our base case is for South32 to soon retest the highs between $4.80 & $4.90, and eventually stage a topside breakout. We maintain a bullish outlook for commodities and base metals, where S32 is well-positioned”

South32 has, since our last update, consolidated constructively just below the four-year highs above $4.90. S32 has recovered from a correction that ensued in March, and upward momentum has since resumed. We believe it is only a matter of time before South32 breaks through the highs between $4.80 & $4.90 and eventually stages a topside breakout to a new record above $5.42. We maintain a bullish outlook for commodities and base metals, where S32 is well-positioned across a range of base metals, including copper, aluminium, alumina, and silver.

Trading Update

South32’s latest strategy and business update paints the picture of a company with solid foundations and appealing long‑term growth options in the right metals, but one that has just delivered a painful reality check on project execution in Arizona. Management is leaning into copper, zinc and silver – metals tied closely to electric vehicles, renewable energy and modern infrastructure – while existing alumina, aluminium and manganese operations provide strong cash flow today, yet the sharp cost increase at the Hermosa project’s Taylor deposit in the US means the share price now reflects both the upside and the scars. For a non‑specialist investor, this combination suggests that the story is attractive over a number of years, but the near‑term risk‑reward looks balanced.

The business update released in mid‑May sets out the core of the current strategy. South32 describes itself as having “reliable operating performance” that provides a platform for growth in base metals, with strong cash generation recently boosted by higher prices for copper, silver and aluminium and a clear plan to grow output of copper, zinc and silver over the rest of the decade. The company expects first production from Taylor – the centrepiece of its Hermosa project in Arizona – in the second half of its 2028 financial year, with a multi‑decade operating life, while it also pursues smaller expansion projects at existing operations and early‑stage options in North and South America, Africa and Australia.

Source: S32 Strategy Update

Source: S32 Strategy Update

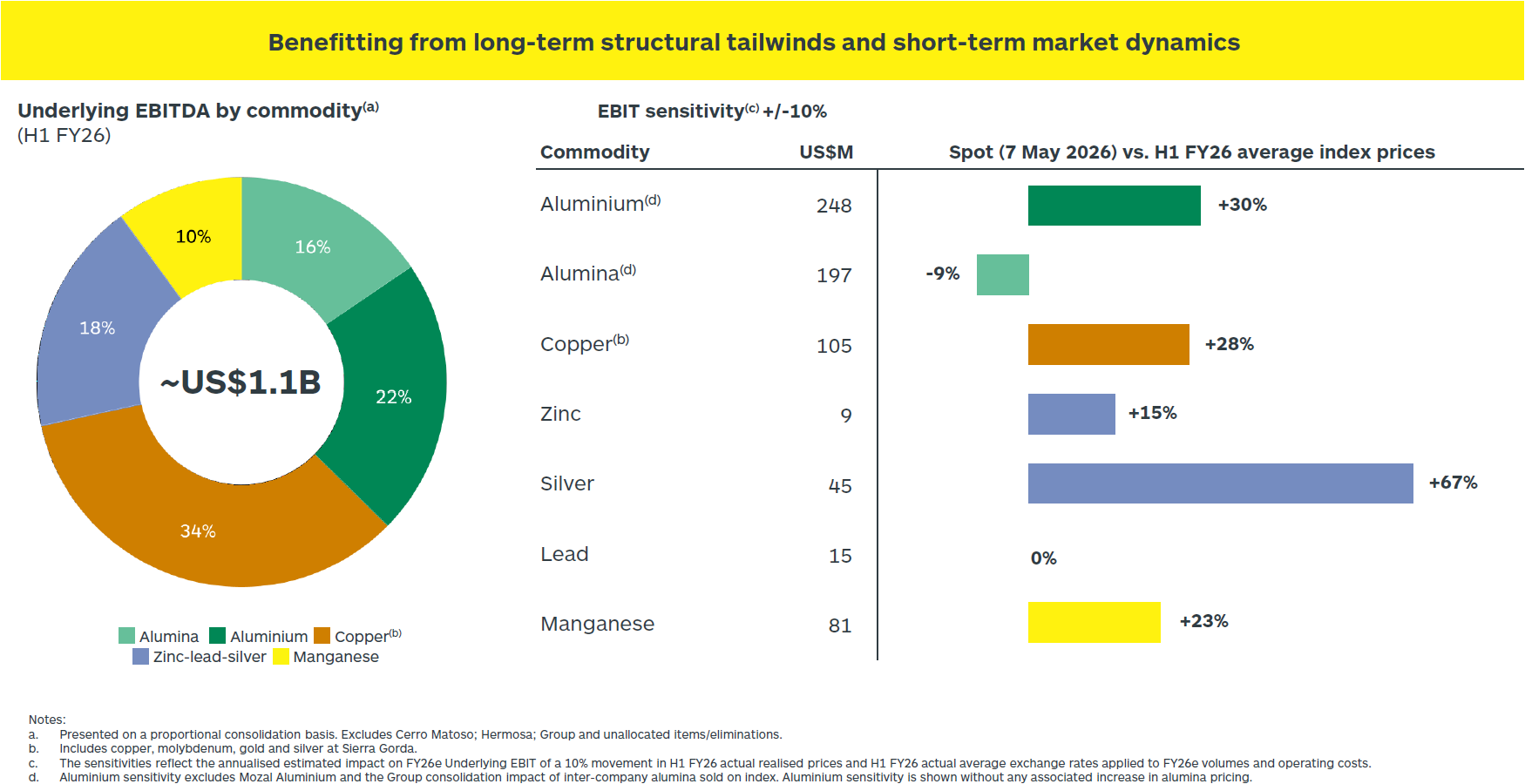

The portfolio is deliberately weighted towards what South32 sees as “energy transition” materials. A recent slide from the update shows that, on a proportional basis, about 34% of underlying cash earnings in the first half of the 2026 financial year came from copper and related by‑products, 18% from zinc, lead and silver, and 10% from manganese, with the remainder from alumina and aluminium, and sensitivity analysis suggests that a 10% move in prices has the biggest impact on earnings in aluminium, alumina, copper and manganese. In plain language, this means the business is now much less dependent on older bulk commodities such as thermal coal, and far more exposed to metals where demand is expected to rise as grids are upgraded, renewable power is rolled out and data centres and electric vehicles multiply.

Source: S32 Strategy Update

The company is not shy about how it sees the market backdrop. In the same presentation it argues that copper demand could increase by close to 30% between 2025 and 2035, driven by renewable energy, power lines, data centres and electric vehicles, and that the world will need the equivalent of roughly three Taylor‑sized zinc projects each year for the next decade to meet expected zinc demand, given current tight supply and low inventories. This view – that there is a looming supply gap in both metals – underpins South32’s decision to focus its growth capital on Taylor and its broader Hermosa district, the Ambler joint venture in Alaska and a suite of copper and zinc exploration partnerships in the US, Canada, Argentina and Africa.

However, the recent cost and schedule shock at Taylor shows how difficult it can be to turn that thematic opportunity into shareholder value. On 29–30 April, South32 disclosed that first‑stage capital costs for Taylor have jumped by more than 50% to about US$3.3 billion from the US$2.2 billion estimate published in a 2024 feasibility study, and that first production has slipped by around a year to the second half of FY28, with full output now expected in FY31 instead of FY30. Media reports note that annual ongoing capital spending has moved up from roughly US$36 million to US$50 million and that forecast unit operating costs have risen from about US$86 per tonne of material processed to about US$100, with the company blaming contractor under‑performance, slower productivity, changes to project scope, inflation and trade tensions for the blow‑out; the internal rate of return is now pitched around 19%, down from 22% previously, still healthy but clearly lower than investors had banked on.

The market reaction was swift. Shares fell by about 5–6% to a little over A$4 immediately after the announcement, wiping close to A$1 billion from the company’s value in a day, and several analysts trimmed their valuation and target prices while keeping neutral ratings, arguing that the cost rise and delay reduce near‑term cash flow and make the project “essentially break‑even” under more conservative price assumptions. Critics also highlighted that this is not the first time the project’s price tag has grown – a chart widely shared on social media shows indicative capital costs rising from around US$1.3 billion in an early study to close to US$3.3 billion now – and warned that execution issues at a critical ventilation shaft still are not fully resolved.

Set against this, South32 has continued to emphasise what has improved at Hermosa. The same update that revealed the higher costs also highlighted a 52% increase in the amount of metal expected to be mined over Taylor’s life and a 10% increase in the broader resource, extending the expected operating life from roughly 28 years to about 33 years; the adjacent Peake copper deposit has also seen a 32% increase in its estimated metal endowment, and management is studying how to feed Peake’s copper into Taylor’s processing plant with only a modest extra circuit, which could add future copper output without a major new build.

Away from Hermosa, the rest of the business gives both support and diversification. The strategy update stresses that operations in Australia, South Africa and South America have been performing reliably, generating strong cash flows supported by firmer prices for key products; at the same time, the company has idled its Mozal aluminium smelter in Mozambique, which had become loss‑making in a difficult power and price environment, demonstrating a willingness to cut underperforming assets rather than chase volume at any cost. South32 also points to a long list of smaller “brownfield” projects – essentially extensions and upgrades at existing sites – such as new mining areas at Worsley alumina, underground extensions at Cannington, and expansion of Australian manganese operations, all of which are intended to deliver extra volume into attractive markets at relatively modest risk compared with building completely new sites from scratch.

The company’s balance sheet and capital allocation record add another layer of comfort. Management notes that since 2016 South32 has allocated about US$19.6 billion across capital spending, acquisitions, ordinary dividends, share buy‑backs and exploration while still keeping a strong balance sheet and an investment‑grade credit rating, and that it continues to target paying out at least 40% of underlying earnings as ordinary dividends while funding growth and opportunistic buy‑backs. That means even with the Hermosa blow‑out, the group is not in a position where it has to issue new shares or take on excessive debt to fund its projects, which is often where value destruction happens for mining‑sector shareholders.

In recent months, stronger metal prices have helped the share price recover some ground. Commentary earlier in the year pointed out that South32’s stock had broken through multi‑year resistance levels as copper, aluminium and manganese prices rallied, and that some investors saw it as one of the more overlooked base‑metals names on the Australian market given its diversified mix and US‑linked growth options; however, valuation pieces published since then suggest that after this rally, the shares are trading at or slightly above many estimates of fair value, particularly once the revised Hermosa numbers are factored in.

Summary

South32 has a proven portfolio of cash‑generating operations in alumina, aluminium and manganese, strong exposure to copper, zinc and silver at a time when demand for these metals is expected to grow, a deep pipeline of growth options from Hermosa and Ambler to various exploration partnerships, and a disciplined approach to balance‑sheet management and dividends.

On the other hand, the Hermosa cost blow‑out and delay have dented confidence in management’s ability to deliver major projects on budget, near‑term free cash flow will be lower than previously expected, and the share price already reflects some of the base‑metals optimism, with several analysts describing the stock as fairly valued at best after its recent rally.

On balance, existing holders may be comfortable staying invested to capture the long‑term upside from copper and zinc growth, but prospective buyers might reasonably wait for either a pull‑back in the share price or firmer evidence that Hermosa’s execution challenges are under control before taking a more aggressively bullish position.

We maintain our HOLD rating on South32 (ASX: S32, LSEG: S32). For those already positioned, South32 remains a core minerals holding, well-placed to ride the next wave of global metals demand and battery supply chain reconfiguration.

Disclosure: Interests associated with Fat Prophets hold shares in South32.