Guidance Upgraded to the Top of the Range

Vicinity’s (ASX: VCX) shopping centre portfolio is performing well, with occupancy at 99.6%, retailer sales up 5.1% and full-year earnings guidance upgraded to the top of its target range. The company has bought full ownership of a Brisbane city centre property for $212 million, backed by $27 billion of government infrastructure ahead of the 2032 Olympics. A new luxury retail precinct at Chatswood Chase in Sydney opens from the fourth quarter. Asset sales at an 18% premium to book value are funding this growth while keeping borrowings at just 26.3% of the portfolio’s value in our view.

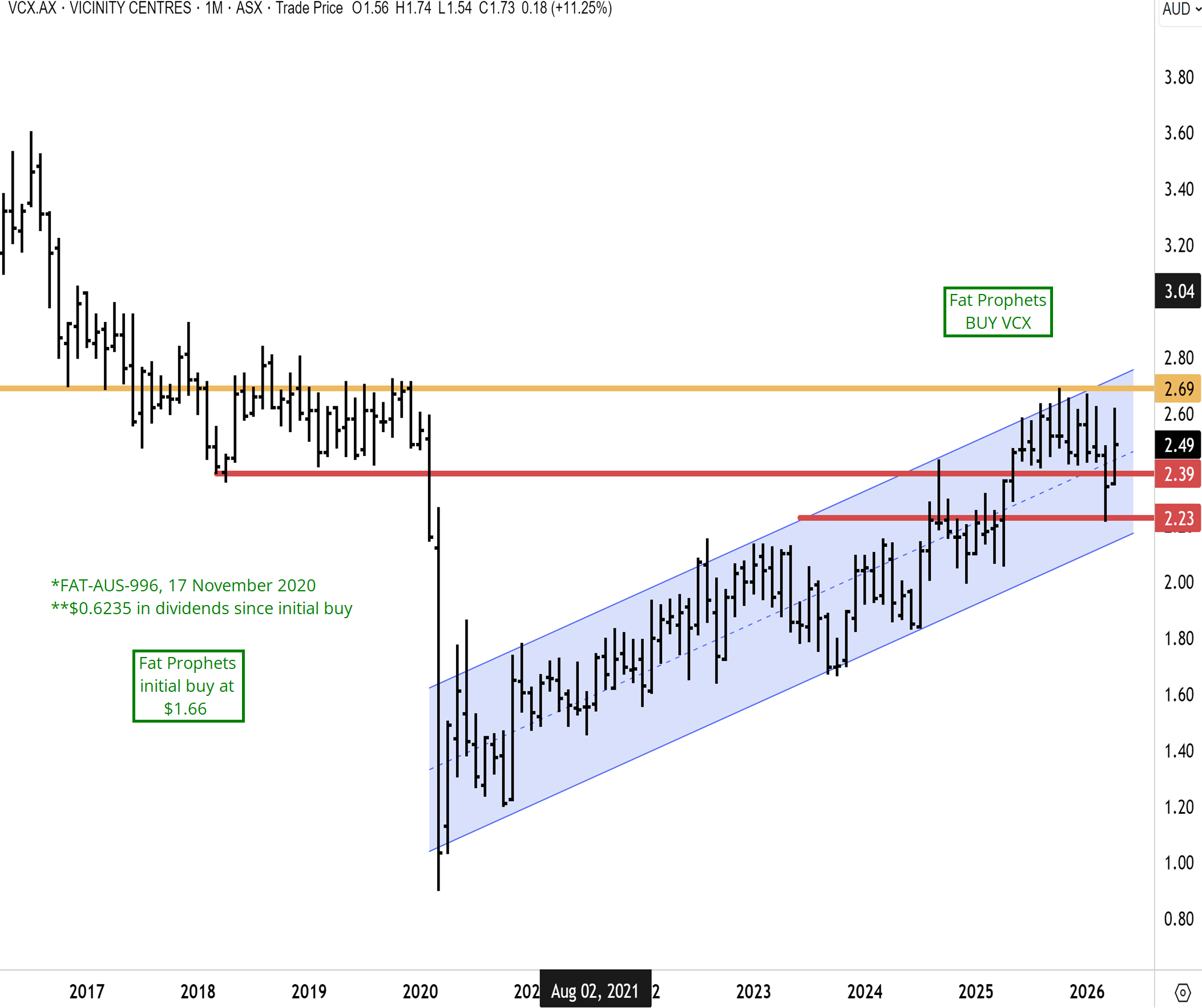

Before the RBA hikes began, in mid-November, we said, “Similar to other REITs, Vicinity has confirmed a breakout above $2.40 and extended upwards to five-year highs above $2.60. We believe the advance is sustainable with the RBA now in an easing cycle, and commercial property prices are likely at an inflection point. We anticipate VCX to retest the highs above $3.40 and the next resistance cluster at $3 in 2026.”

Since our last update back in November, much has changed at the RBA in terms of rate settings, with the central bank pivoting to a tightening bias. This has been a headwind for the REIT sector. Vicinity has, however, remained constructively within a well-defined upward trend channel on the 10yr chart below. Despite a selloff in March, Vicinity has managed to rebound and hold above the breakout level near the defining resistance level at $2.40. We believe the uptrend channel in VCX is durable and sustainable. We anticipate VCX to retest this year’s highs above $2.69 sometime this year, and in time, the next resistance cluster above $3.

Trading Update

Vicinity’s latest interim result and subsequent announcements support a measuredly positive long‑term view: earnings and asset values are growing, the portfolio is skewing further towards premium centres, and key development projects are progressing, all while balance‑sheet risk remains contained despite a higher‑for‑longer rates backdrop. The numbers show consistency and Vicinity is quietly building a higher‑quality, more resilient earnings base rather than relying on one‑off valuation gains or aggressive leverage to deliver growth.

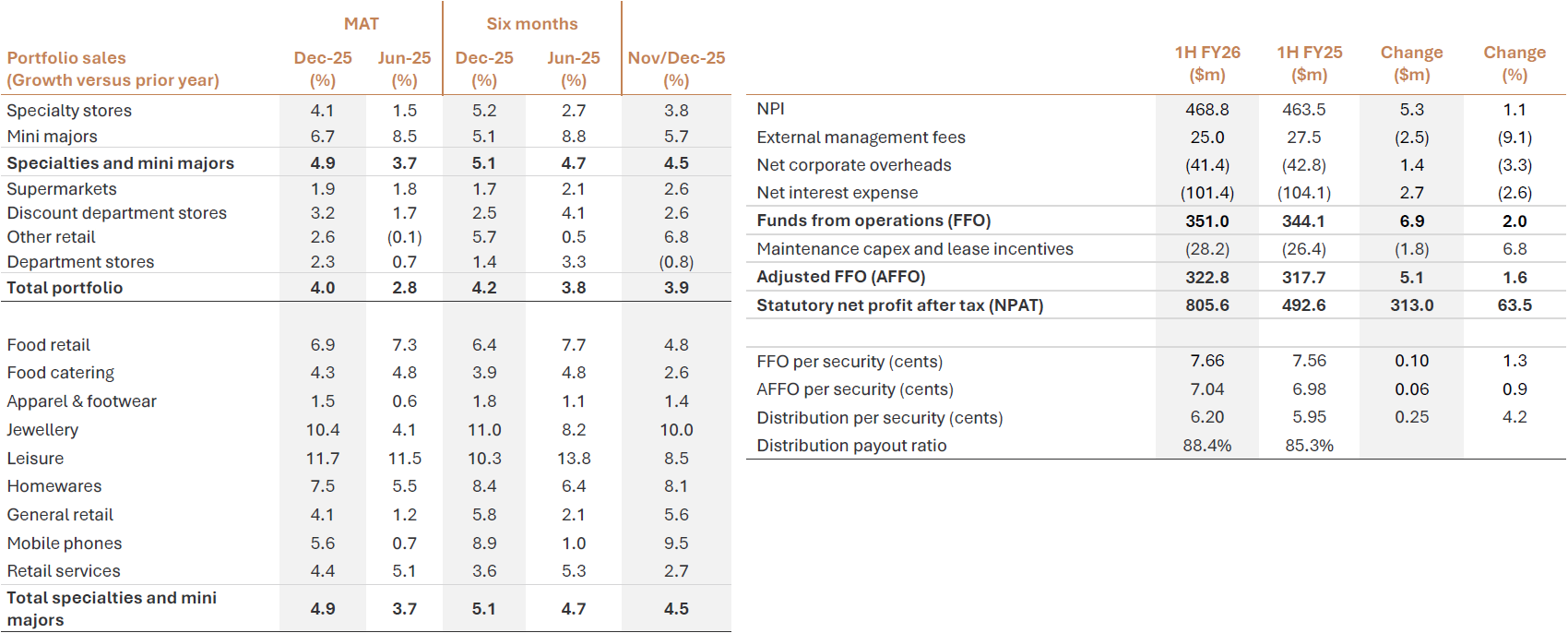

For the six months to 31 December 2025, Vicinity delivered statutory NPAT of $805.6 million, up from $492.6 million a year earlier, supported by both higher Funds From Operations (FFO) and another period of valuation gains across the portfolio. FFO per security rose 1.3% to 7.66 cents, and by 4.1% when adjusted for one‑off transaction items and lower lost rent from developments, while comparable net property income grew 3.7% – or 4.1% excluding new and increased taxes and levies – reflecting the underlying strength of leasing and rent metrics.

Income growth is increasingly underpinned by premium assets and a very tight operating profile. Specialty and mini‑major sales increased 5.1% in the half, total portfolio retail sales rose 4.2% on a comparable basis, and specialty sales productivity climbed 3% to $13,425 per square metre, with portfolio occupancy edging up to 99.6%, leasing spreads at +4.6% and average annual escalators on new deals at +4.7%, supporting both current rents and future re‑leasing power.

Source: VCX 1H26 Presentation

Source: VCX 1H26 Presentation

Strategically, Vicinity has accelerated its tilt toward higher‑quality assets. Premium centres – Chadstone, outlet centres, CBDs and premium regionals – now comprise 66% of portfolio value, up from 51% in June 2022, and on a pro‑forma basis the total portfolio value has increased by 12.6% over that period despite a net reduction of 12 lower‑quality assets and a 20‑basis‑point expansion in the weighted average capitalisation rate to 5.5%, implying that income growth and capital spend have outweighed headwinds from yields.

A cornerstone of that strategy is taking full control of Brisbane’s Uptown on Queen Street Mall for $212 million, buying out IFM Investors’ 75% stake in a centre Vicinity has managed for decades. Management highlights that Uptown sits in a trade area benefitting from around $27 billion of state‑funded infrastructure ahead of the 2032 Olympics, and that securing 100% ownership will allow it to execute a $300–350 million redevelopment that aims to emulate the Emporium Melbourne model – a full‑price, experience‑led CBD destination in a market with limited comparable supply.

Crucially, this acquisition is being funded through disciplined capital recycling rather than stretching the balance sheet. Since FY24 Vicinity has divested about $1.0 billion of non‑strategic assets, including recent agreements to sell Gympie Central, Whitsunday Plaza, Armidale Central, Victoria Park Central and ancillary land parcels for a combined $327 million at an 18.2% premium to June 2025 book values, helping to keep gearing at 26.3% – the lower end of the 25–35% target range – while freeing capital for premium‑asset developments.

Development execution continues to reinforce the earnings story. At Chadstone, the Market Pavilion fresh‑food precinct and the One Middle Road office tower are complete, with the latter fully occupied from January 2026 by Adairs and Kmart headquarters, adding about 2,000 office workers and taking total weekday office population above 6,500, while Hotel Chadstone now hosts close to 110,000 visitors per year, deepening the precinct’s mixed‑use, destination appeal.

Chatswood Chase is emerging as the flagship example of Vicinity’s premium repositioning. Stage 1 of the reimagined centre opened in October 2025 and attracted 2.4 million visitors and $119 million of retail sales in the December quarter, in line with expectations, while Stage 2 – a new luxury precinct anchored by more than 20 high‑end brands – is on track for opening from 4Q FY26 and is expected to cement the centre’s status as the leading retail destination on Sydney’s north shore.

The development pipeline extends beyond retail. Vicinity is advancing mixed‑use residential concepts at Chatswood Chase and Bankstown Central that together contemplate nearly 2,000 apartments across roughly 27,500 square metres of land, with both sites endorsed for the NSW State Housing Development Authority’s accelerated assessment pathway, giving Vicinity optionality to unlock value from air‑rights and surplus land in ways that complement, rather than cannibalise, the underlying retail.

Management confidence in near‑term earnings is reflected in upgraded guidance. Vicinity now expects FY26 FFO and Adjusted FFO per security to land around the top end of its 15.0–15.2 cent and 12.8–13.0 cent ranges, respectively, and has nudged comparable NPI growth guidance up to about 3.5% from 3.0%, while signalling a full‑year distribution payout ratio within the 95–100% of AFFO target range and maintaining a weighted average cost of debt guidance of roughly 5.0%, slightly below FY25’s 5.1% despite the ongoing rates reset.

The macro backdrop is not without risk, but it is arguably more supportive for prime retail landlords than for many other rate‑sensitive sectors. Australia’s latest inflation prints have surprised to the upside on some measures, keeping the possibility of further RBA tightening alive, yet first‑quarter data also show underlying inflation easing from prior peaks even as headline price growth hits a two‑year high, suggesting that while funding costs may stay elevated, real income growth and population gains should continue to support discretionary spending and retailer sales in well‑located centres like those in Vicinity’s portfolio.

Summary

Vicinity Centres is growing NPAT and FFO modestly but consistently, directing capital from non‑core assets into premium centres and high‑return redevelopments, maintaining near‑record occupancy and positive leasing spreads, and signalling that FY26 FFO and AFFO will come in at the top of guidance, all while keeping gearing conservative and building optionality through mixed‑use and CBD‑luxury projects; in a world where higher rates and sticky inflation will likely punish weaker malls and over‑levered landlords, that combination of resilient cash flows, visible reinvestment levers and disciplined balance‑sheet management makes Vicinity’s current yield and asset‑backed growth profile look attractive for patient, income‑oriented equity holders who can look through short‑term rate volatility and cyclical swings in consumer sentiment.

We maintain our BUY rating on Vicinity Centres (ASX: VCX) especially for Members without exposure. The company remains a solid addition for Members seeking exposure to Australia’s most resilient shopping centre operator, supported by quality, scale, and a clear roadmap for future growth.