Alumina Hits a Record as the Weather Hits Manganese

South32’s (ASX: S32, LSEG: S32) March quarter delivered a mixed but broadly solid result. Brazil’s alumina plant reached a record year-to-date output, and a net cash position was established despite US$158 million spent on a major zinc project in Arizona. However, weather disruptions and a cyclone led to a 6% cut to full-year manganese production guidance in Australia. Most other production guidance was maintained.

We are watching the impact of rising freight, fuel and chemical costs on margins.

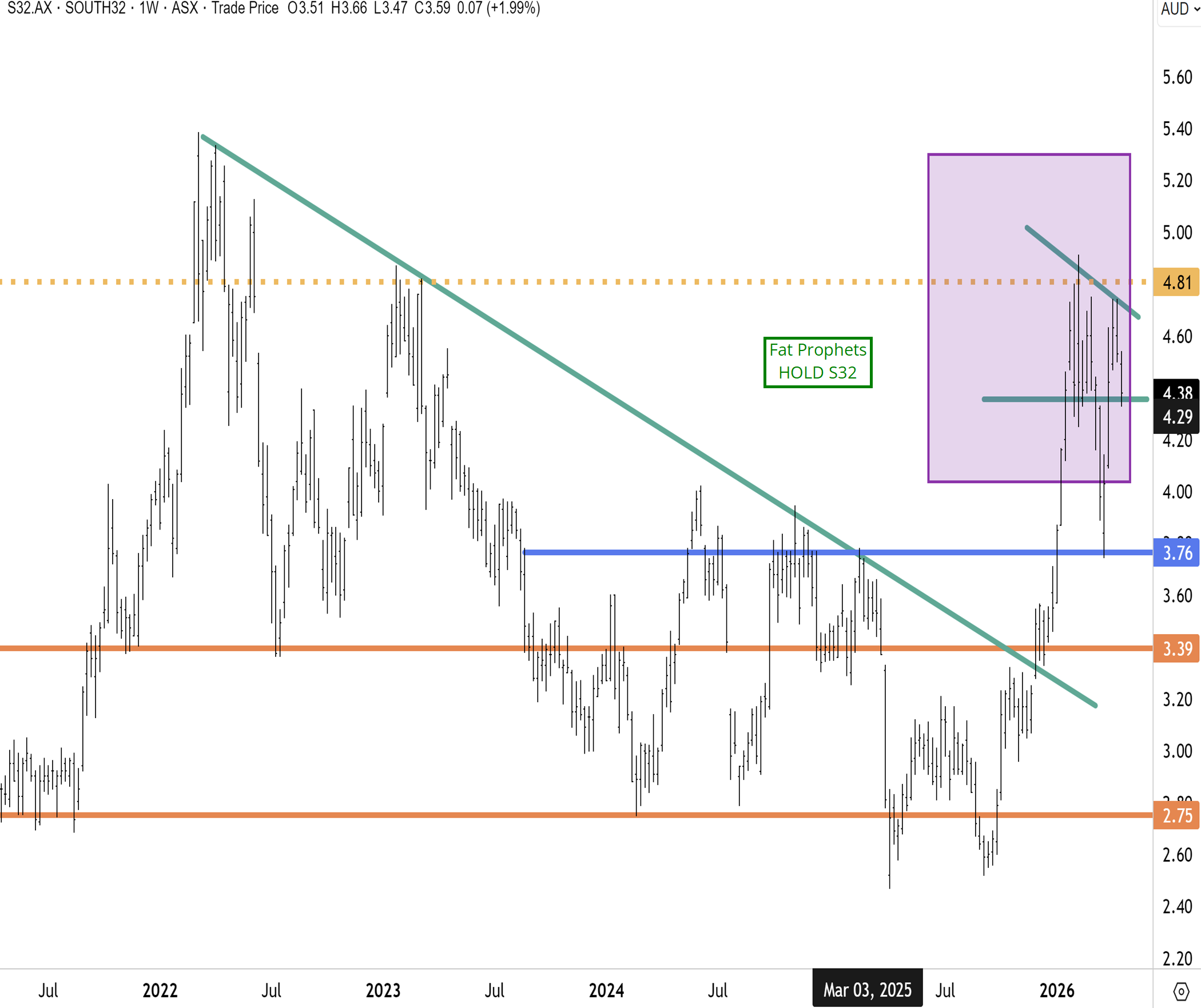

In our last tech update on the 18th of March, we noted that “After surging to four-year highs above $4.90, South 32 has corrected lower in what has been a ‘risk off’ environment for global stock markets. We believe the correction is close to ending with strong support near $4 (being the breakout level) now within proximity. We believe South32 will recover strongly when global risk appetite returns. We maintain a bullish outlook for commodities and base metals, where S32 is well-positioned.”

South 32 continues to consolidate after surging to four-year highs above $4.90 back in February. While S32 corrected lower in March, it was a ‘risk off’ environment for global stock markets, and upward momentum has since resumed. We believe the correction that unfolded last month is close to ending. Our base case is for South32 to soon retest the highs between $4.80 & $4.90, and eventually stage a topside breakout. We maintain a bullish outlook for commodities and base metals, where S32 is well-positioned

Trading Update

South32’s March quarter shows a group delivering generally solid production and cash generation, absorbing adverse weather and cost headwinds, while making a selective downgrade to Australian manganese guidance and keeping the rest of the portfolio broadly on track. The picture that emerges is neither obviously weak nor clearly exciting: aluminium and alumina are steady to slightly better on a year‑to‑date basis, Hermosa continues to advance, but weather, freight and input‑cost pressures are real and the near‑term risk‑reward looks finely balanced rather than compellingly skewed either way.

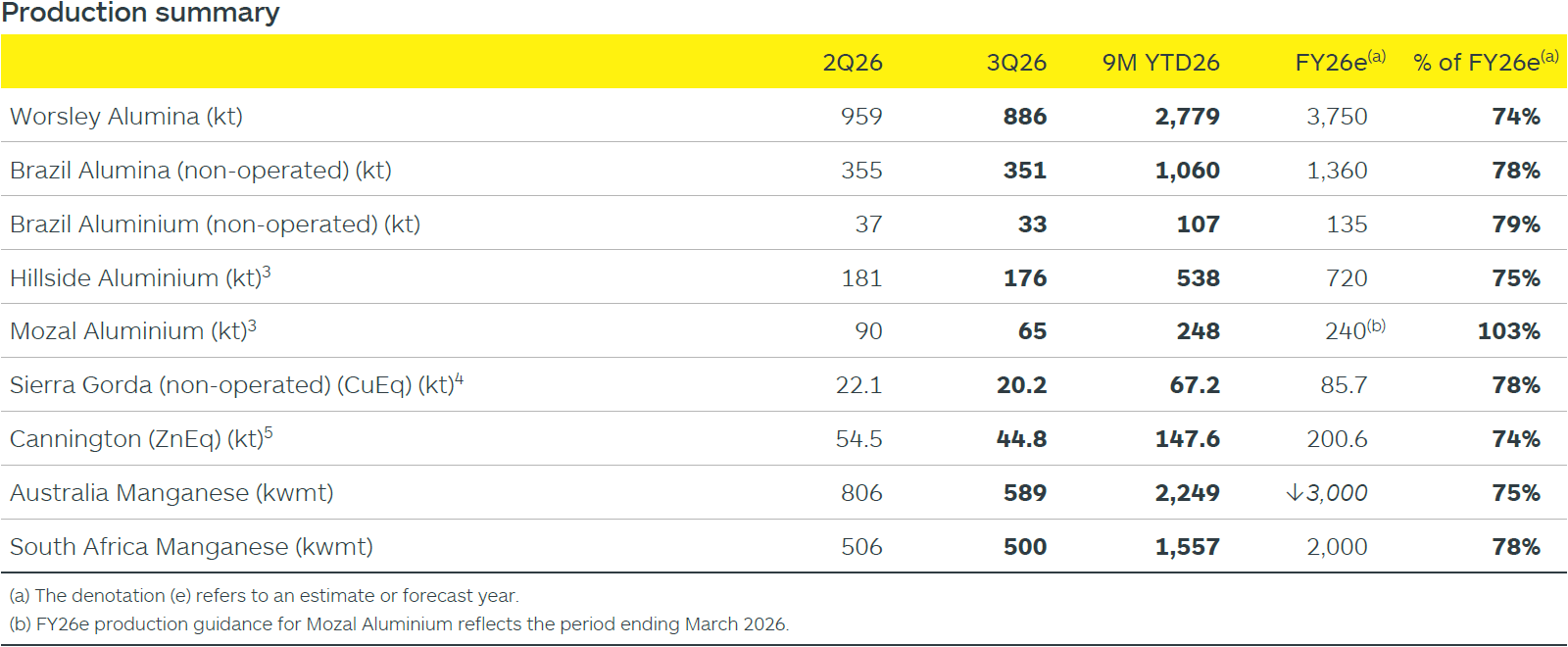

Operationally, the quarter was mixed but within expectations. Year to date, alumina production is up 1% with Brazil Alumina at a record 1,060 thousand tonnes, while Worsley Alumina is broadly flat at 2,779 thousand tonnes despite Tropical Cyclone Narelle disrupting gas supply and plant availability; aluminium production is “largely unchanged” versus the prior period, with Hillside Aluminium continuing to test its maximum technical capacity and Brazil Aluminium 7% higher year on year at 107 thousand tonnes. Against that, Worsley’s March‑quarter alumina output fell to 886 thousand tonnes from 959 thousand tonnes in 2Q26 and Brazil Aluminium’s quarterly production dipped 11% to 33 thousand tonnes, reflecting earlier pot outages, prompting headlines that the company had logged “lower fiscal Q3 Worsley Alumina and Brazil Aluminium production” even as full‑year guidance remained intact.

The manganese business illustrates both the cyclical leverage and the weather risk. Australia Manganese production jumped to 2,249 thousand wet metric tonnes (kwmt) in the nine months to March 2026 as operations fully recovered from Tropical Cyclone Megan, more than three times the prior‑year comparative, but March‑quarter output fell 27% quarter on quarter to 589 kwmt as elevated water levels, wet‑season rainfall and Cyclone Narelle again constrained operations, leading South32 to cut FY26 production guidance by 6% to 3,000 kwmt. By contrast, South Africa Manganese production was broadly unchanged year on year at 1,557 kwmt and up 5% versus 3Q25, with FY26 guidance of 2,000 kwmt reaffirmed, underlining that the group has some geographic diversification even if the Australian operation remains the key swing factor for volumes and price exposure.

Source: S32 3Q26 Filing

Source: S32 3Q26 Filing

Despite those disruptions, news flow over the past few months has highlighted that manganese output is still much stronger than it was a year ago. External coverage in January and again this week noted that South32 had previously posted a near‑17% rise in quarterly manganese output as its Australia division normalised post‑Megan, and that second‑quarter output of around 1.3 million wet tonnes from Australia and South Africa combined had lifted the shares to multi‑year highs and allowed management to maintain full‑year guidance at that time. The latest cut to Australia Manganese guidance therefore looks more like a recalibration from a strengthened base in light of fresh weather challenges, rather than a reversal of the broader recovery trend that has been in place since late FY25.

Aluminium remains a relative bright spot, but not without nuance. Hillside Aluminium produced 176 thousand tonnes in the March quarter, 1% above the same period last year and taking nine‑month output to 538 thousand tonnes, essentially flat year on year, as the smelter continued to push against its technical ceiling despite South African load‑shedding; Brazil Aluminium finished the quarter with improved pot stability and output and is described as tracking ahead of its 135 thousand tonne FY26 guidance, even though quarterly production was temporarily lower. However, Mozal Aluminium has transitioned to care and maintenance as planned, with production down 28% quarter on quarter to 65 thousand tonnes and FY26 guidance effectively capped by the March shut‑down, so group aluminium volumes are being maintained through Hillside and Brazil rather than growing, while cost pressures from higher Middle East‑linked freight and caustic soda prices are expected to feed into alumina operating costs if they persist.

In base metals, Sierra Gorda and Cannington had weather‑affected but manageable quarters. Sierra Gorda’s payable copper‑equivalent production was flat year on year at 67.2 thousand tonnes for the nine months and 20.2 thousand tonnes in the March quarter, with heavy rainfall temporarily curbing mining access and processing, yet FY26 guidance of 85.7 thousand tonnes was maintained and the asset delivered a record quarterly distribution of US$135 million to partners. Cannington’s zinc‑equivalent output fell 18% quarter on quarter and 8% versus 3Q25 as lower grades and flooding in north‑west Queensland disrupted operations and third‑party rail access, but management expects higher sales volumes in the June quarter as stockpiled concentrate is railed out, and kept full‑year guidance for zinc‑equivalent production at 200.6 thousand tonnes.

Financially, the group remains in a net‑cash position and continues to fund both shareholder returns and growth. South32 generated US$121 million of net cash in the March quarter, lifting net cash to US$96 million after investing US$158 million in growth capex at Hermosa, while also returning US$35 million via on‑market buy‑backs over the nine months to March and, after quarter‑end, paying a fully franked US$175 million interim dividend for the December 2025 half. Equity‑accounted investments contributed a cumulative US$375 million of net distributions over the nine months – including US$315 million from Sierra Gorda and US$60 million from manganese – supporting free‑cash‑flow generation even as working capital was flat in the quarter due to higher finished‑goods inventories at Mozal and Cannington that are expected to unwind in June.

Hermosa remains the flagship growth project but still carries execution and capital‑discipline risk. The company invested US$496 million of growth capex at Hermosa in the nine months to March, continuing construction of the Taylor zinc‑lead‑silver project and completing the exploration decline at the Clark battery‑grade manganese deposit, and reached a key permitting milestone with the US Forest Service issuing the Final Environmental Impact Statement and Draft Record of Decision under the FAST‑41 framework. South32 plans to complete an updated assessment of Taylor milestones and capital expenditure in the June half as it awards further underground and surface‑infrastructure packages, while also advancing regional exploration that suggests potential continuity between the Peake copper prospect and Taylor Deeps, hinting at additional upside if drilling confirms a larger system.

Set against these positives are some clear headwinds. Beyond the weather‑related cut to Australia Manganese guidance, South32 explicitly flags Middle East conflict‑driven pressures on freight rates, diesel and caustic‑soda prices, noting that if these persist they will push operating unit costs higher across alumina and other businesses; the tragic fatality at Worsley Alumina in March underscores ongoing safety and ESG risks, and the group also acknowledges that stronger producer currencies in key jurisdictions are adding to cost inflation. In aluminium, the closure of Mozal reduces diversification and leaves Hillside more central to group earnings at a time when South African power reliability and cost remain issues, while in base metals both Sierra Gorda and Cannington are facing cost pressure from new labour agreements, energy, and logistics that could squeeze margins if metal prices soften from currently supportive levels.

Summary

South32 offers a diversified exposure to alumina, aluminium, manganese and base metals, backed by a net‑cash balance sheet, ongoing buy‑backs and a progressing Hermosa growth pipeline, but it is also contending with recurring weather disruptions in Australia Manganese, rising freight and input costs linked to Middle East instability, and a portfolio that is maintaining production more than expanding it in aggregate. For existing holders, the case to maintain positions rests on confidence that management will manage these operational and cost risks, deliver Hermosa within an acceptable capital envelope and continue returning surplus cash, while prospective investors may prefer to wait for either a clearer inflection in cost trends and manganese reliability, or a wider valuation discount that more fully compensates for the remaining execution and commodity‑cycle uncertainties.

We maintain our HOLD rating on South32 (ASX: S32, LSEG: S32). For those already positioned, South32 remains a core minerals holding, well-placed to ride the next wave of global metals demand and battery supply chain reconfiguration.

Disclosure: Interests associated with Fat Prophets hold shares in South32.