| Price to Earnings | EV/EBITDA | |

|---|---|---|

| FY1 | 12.1 | 6.4 |

| FY2 | 6.4 |

A Machine Running at Full Throttle

Newmont delivered the most profitable quarter in its 105-year history in Q1. The stock has corrected almost 20% from the peak seen in January, as gold prices have retreated from that surge seen earlier in the year. At the time of writing, gold prices were trading at about $4,620/z, which is 5.7% lower than the average realised price of $4,900/oz enjoyed in Q1. We see scope for a period of consolidation in the gold price before the next leg higher. That view, not any concern about the business itself, is what prompts us to pare our rating to Hold. The operational story remains excellent. Attributable gold production of 1,301 thousand ounces kept Newmont on track for its full-year guidance of 5.26 million ounces, with Q1 representing approximately 24.7% of that annual target – in line with the company’s own seasonality guidance of roughly a 48% H1 weighting. Adjusted net income came in at $3.16 billion, or $2.90 per diluted share, against a Wall Street consensus of $2.18 – a 33% beat that continued Newmont’s streak of six consecutive earnings surprises. Revenue grew 46% year-on-year to $7.31 billion, driven almost entirely by the gold price, with realised copper at $5.68/lb and silver at $66.78/oz providing substantial supplementary lift. HOLD.

Since our last technical update, Newmont surged to new record highs near A$200. Since then, (ASX: NEM) has corrected sharply to $130 before finding strong support at the primary uptrend. Newmont has since rebounded in recent weeks to above $150. We anticipate new record highs to ensue in 2026, with support very well defined now at $130/140 below, in our opinion.

Costs: Great result, but we can expect an increase over the coming quarters

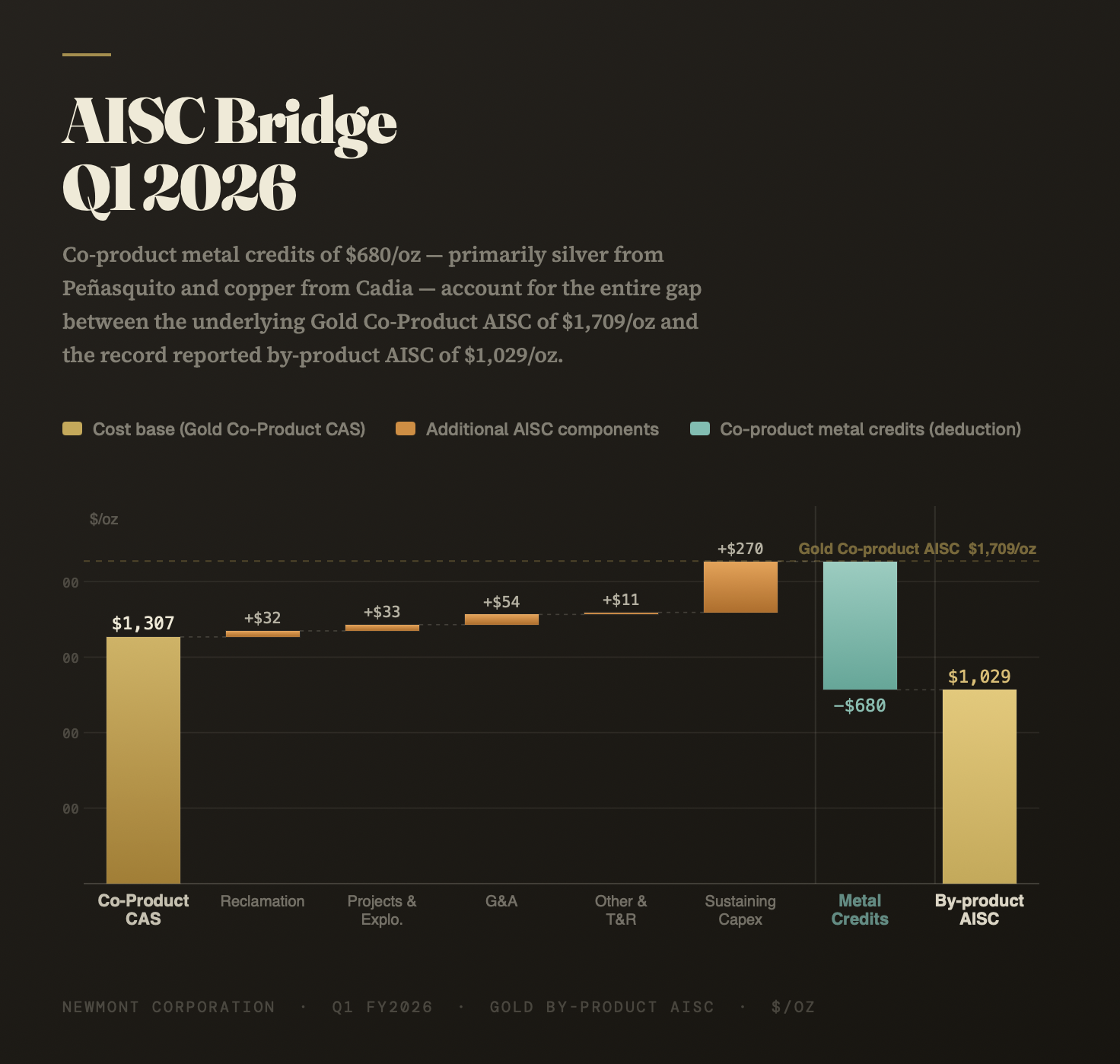

The most exciting number in the release was Gold By-Product AISC of $1,029/oz – company record, but we should understand the underpinnings clearly, rather than automatically extrapolating it forward. AISC is built from a bridge of components. In Q1, gold costs applicable to sales on a co-product basis ran to $1,307/oz. Sustaining capital, G&A, reclamation and other charges added a further $402/oz to reach a Gold Co-Product AISC of $1,709/oz. The transformative element was the deduction of $680/oz in co-product metal credits – largely the silver and copper revenues generated at Peñasquito and Cadia in a quarter when both metals were at favourable levels.

Compounding the effect, Newmont spent only $381 million of its full-year $1,950 million sustaining capital budget in Q1. The company was transparent about this. Sustaining capital spend is explicitly guided to be weighted toward H2, and unit costs are expected to be “notably higher” in Q2. The bills haven’t gone away; they’ve just been deferred. The full-year AISC guidance of $1,680/oz remains unchanged, so we should treat the Q1 number as a seasonal low, not a new baseline.

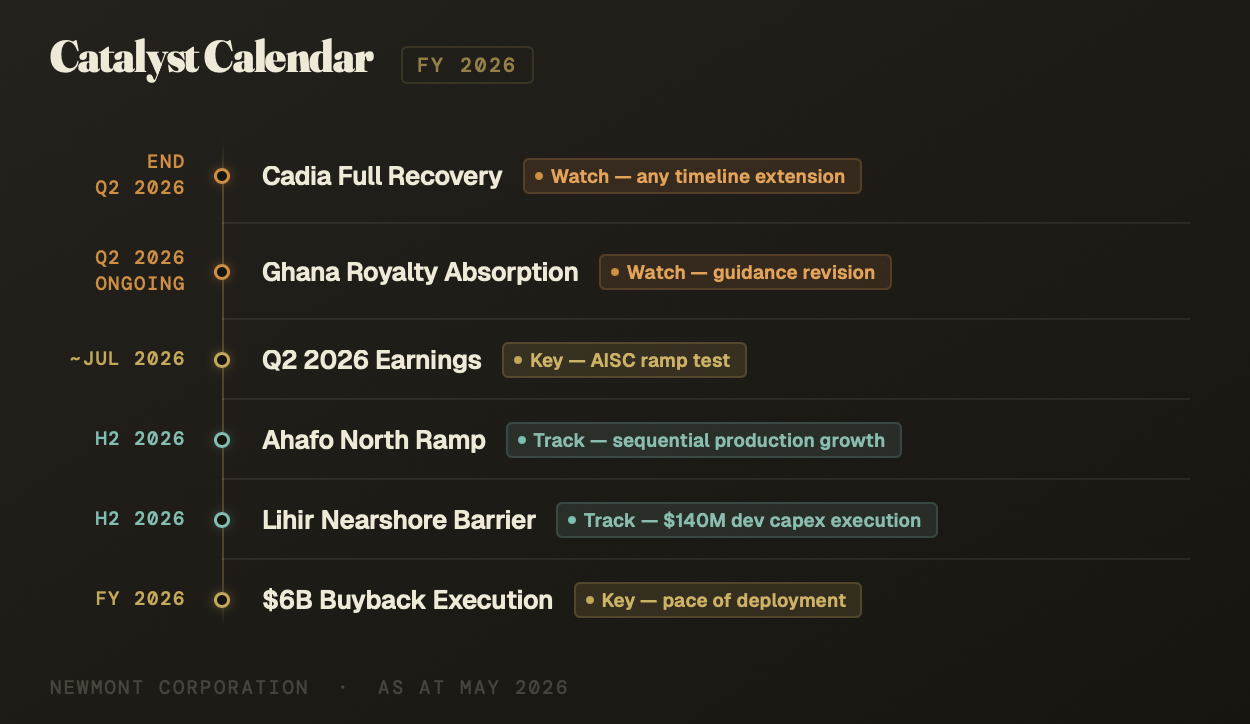

Two further cost headwinds. The Government of Ghana enacted a new sliding royalty in March 2026 – a scale of 5% to 12%, dependent on the gold price – which Newmont estimates will add approximately $185/oz to AISC at its Ahafo operations, or $25/oz across the group. Newmont says it is working to offset the impact through productivity initiatives, and the full-year guidance has not been revised. The market will get its first test of whether that offset is credible when Q2 results land in July. Separately, a magnitude 4.5 earthquake struck near the Cadia operation in New South Wales on 14 April. There were no injuries and no damage to tailings infrastructure, but underground rehabilitation is expected to take approximately five weeks, meaning Q2 production at Cadia will be lower before a return to full capacity by the end of the second quarter.

A Fortress Balance Sheet

For all the noise around cost trajectories, Newmont has established a fortress balance sheet. Free Cash Flow of $3.14 billion in a single quarter is a record for the company. Cash on the balance sheet stood at $8.78 billion at quarter-end, against total debt of $5.08 billion, resulting in a net cash position of $3.24 billion. Total liquidity, including the undrawn revolving credit facility, reaches $12.8 billion. Even under a severe stress scenario, the company would remain net cash.

Capital returns were substantial. Newmont repurchased $1.895 billion of stock in the first quarter alone, fully exhausting the previous $6 billion authorisation and triggering a new $6 billion buyback program from the Board. The quarterly dividend of $0.26 per share (US$1.04 annualised) was maintained.

Summary

The operational case for owning Newmont (ASX, US: NEM) remains intact. As the only pure-play gold producer in the S&P 500, Newmont occupies a structurally unique position: it is the default vehicle for institutional investors seeking index-eligible gold mining exposure. The company has a $3.2 billion net cash cushion, a $6 billion buyback program in motion, and a cost structure that, even allowing for the Q2–Q4 ramp, will still yield hefty AISC margins. On a forward basis, the stock trades at 6.4 times NTM EV/EBITDA and 12.1 times NTM P/E, with a PEG ratio of 0.3, all of which are attractive given our expectations about the metals pricing deck going forward.

The rating change is largely a commodity positioning call. Gold has retreated from its January record, with the US-Iran conflict and disrupted Strait of Hormuz shipping introducing oil-price pressure that is complicating the Federal Reserve’s path. We are not forecasting a significant further decline in gold, but we do see a consolidation phase before the next structural move higher, and we would rather hold current positions at current prices than add into that period of uncertainty. When the gold price picture clarifies – or if the stock re-rates to a level that compensates adequately for near-term commodity risk – we will revisit our rating. Existing holders should sit tight. The business does not warrant reducing exposure – unless gold, silver, and PGM positions have come to represent an outsized share of the overall portfolio, in which case trimming to a more comfortable weighting is a reasonable response to the current consolidation rather than a reflection on Newmont’s underlying quality. HOLD.

Disclosure: Interests associated with Fat Prophets hold shares in Newmont.